The following is a periodic analysis of world oil production conducted by Ace at The Oil Drum. It is a comprehensive report of the state of crude oil, and other petroleum liquids, production. The upshot is:

- World crude oil production has likely peaked based on production data as well as socio-geopolitical factors.

- The possibility of higher future peaks is constrained by geology (production decline rates) and economics (investment in new oil discovery and drilling due to economic stresses).

My reasons for posting this long article here are two:

- I consider this the finest analysis Ace has done to date and

- I consider it vital for people to understand the depth and breadth of the challenges ahead.

Many thanks to Ace and The Oil Drum.

World Oil Production Forecast - Update May 2009

Posted by ace on May 19, 2009 - 10:59pm

Topic: Supply/Production

Tags: colin campbell, iea, jean laherrère, non-opec, oil production forecast, opec, original, peak oil, total liquids [list all tags]

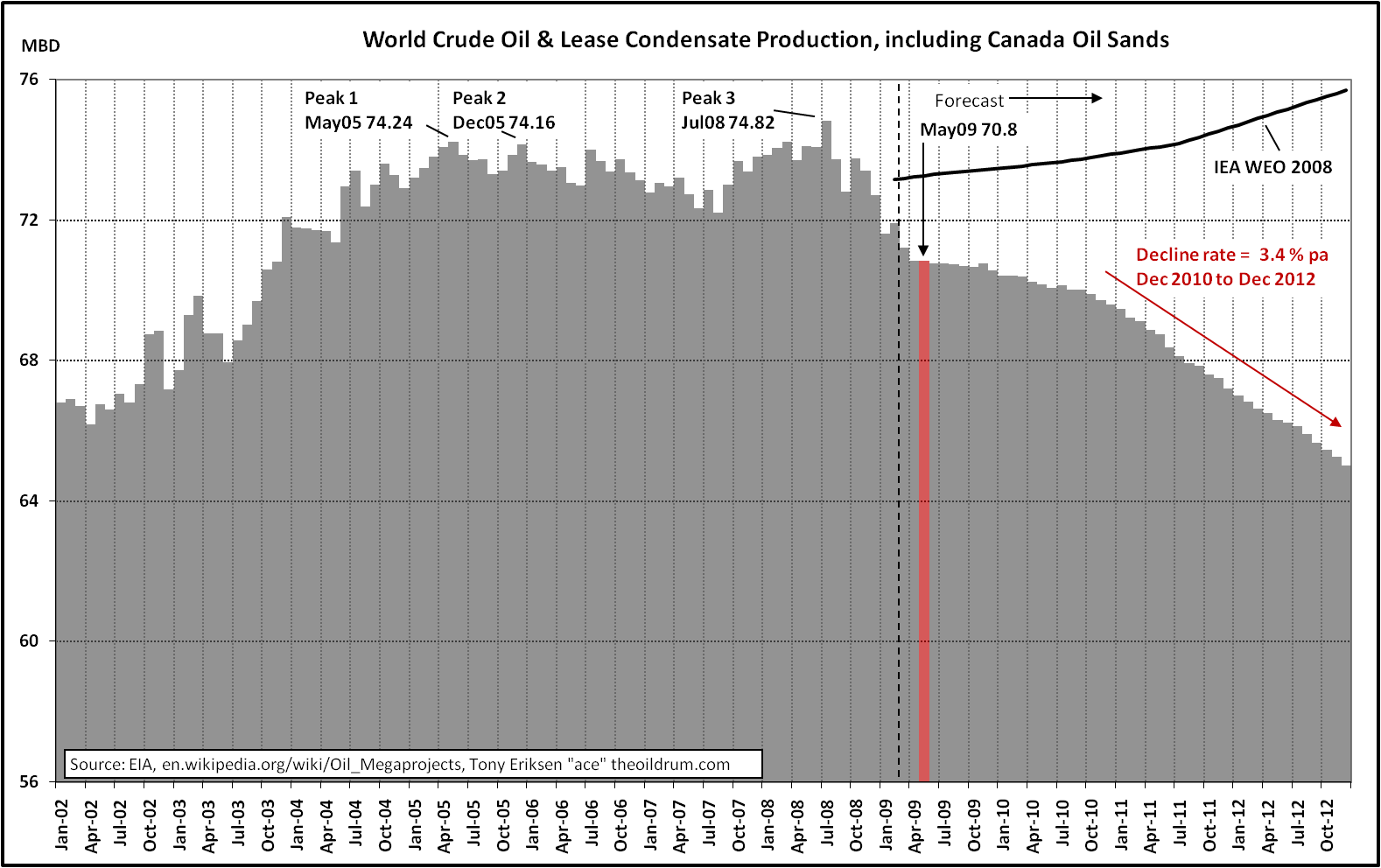

World oil production peaked in July 2008 at 74.82 million barrels/day (mbd) and now has fallen to about 71 mbd. It is expected that oil production will decline slowly to about December 2010 as OPEC production increases while non-OPEC production decreases. After 2010 the resulting annual production decline rate increases to 3.4% as OPEC production is unable to offset cumulative non-OPEC declines. The forecast from the IEA WEO 2008 is also shown for comparison.

The US Energy Information Administration (EIA) and the International Energy Agency (IEA) should make official statements about declining world oil production now to renew the focus on oil conservation and alternative renewable energy sources.

World Oil Production

World crude oil, condensate and oil sands production peaked in 2008 at an average of 73.78 million barrels per day (mbd) which just exceeded the previous peak of 73.74 mbd in 2005, according to recent EIA production data. Production is expected to decline further as non OPEC oil production peaked in 2004 and is forecast to decline at a faster rate in 2009 and beyond due mainly to big declines from Russia, Norway, the UK and Mexico. Saudi Arabia's crude oil production peaked in 2005. By 2011, OPEC will not have the ability to offset cumulative non OPEC declines and world oil production is forecast to stay below its 2008 peak.

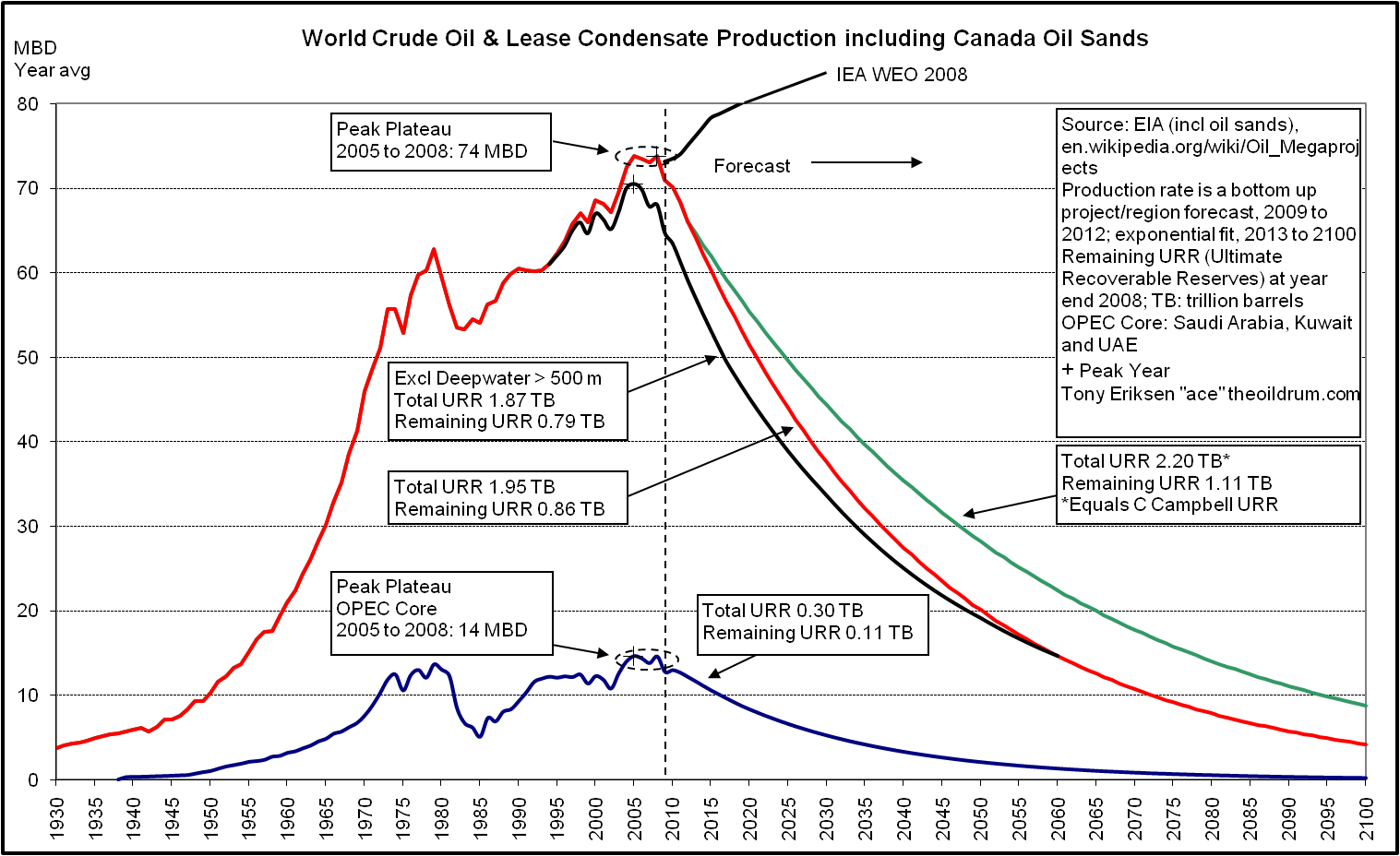

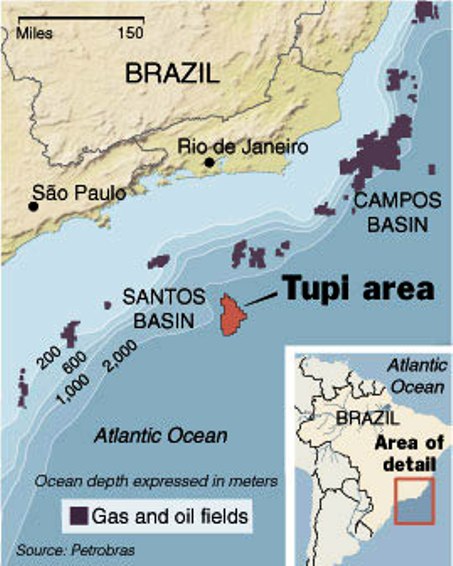

My estimate of 1.95 trillion barrels (TB) of total Ultimate Recoverable Reserves (URR) of oil is used to generate the forecast shown by the red line below. If Colin Campbell's estimate of 2.20 TB is used, which is 250 billion barrels (Gb) greater than my estimate due mainly to more optimistic assumptions about OPEC reserves, the peak production date remains at 2008. This shows that an additional 250 Gb of recoverable oil reserves does not change the peak oil date and instead increased production rates occur later as indicated by the green line below. Additional reserves and the related production from prospective areas such as the arctic, Iraq, and Brazil's Santos basin are highly unlikely to produce another peak but should decrease the production decline rate after 2012.

![]()

World Liquids Production

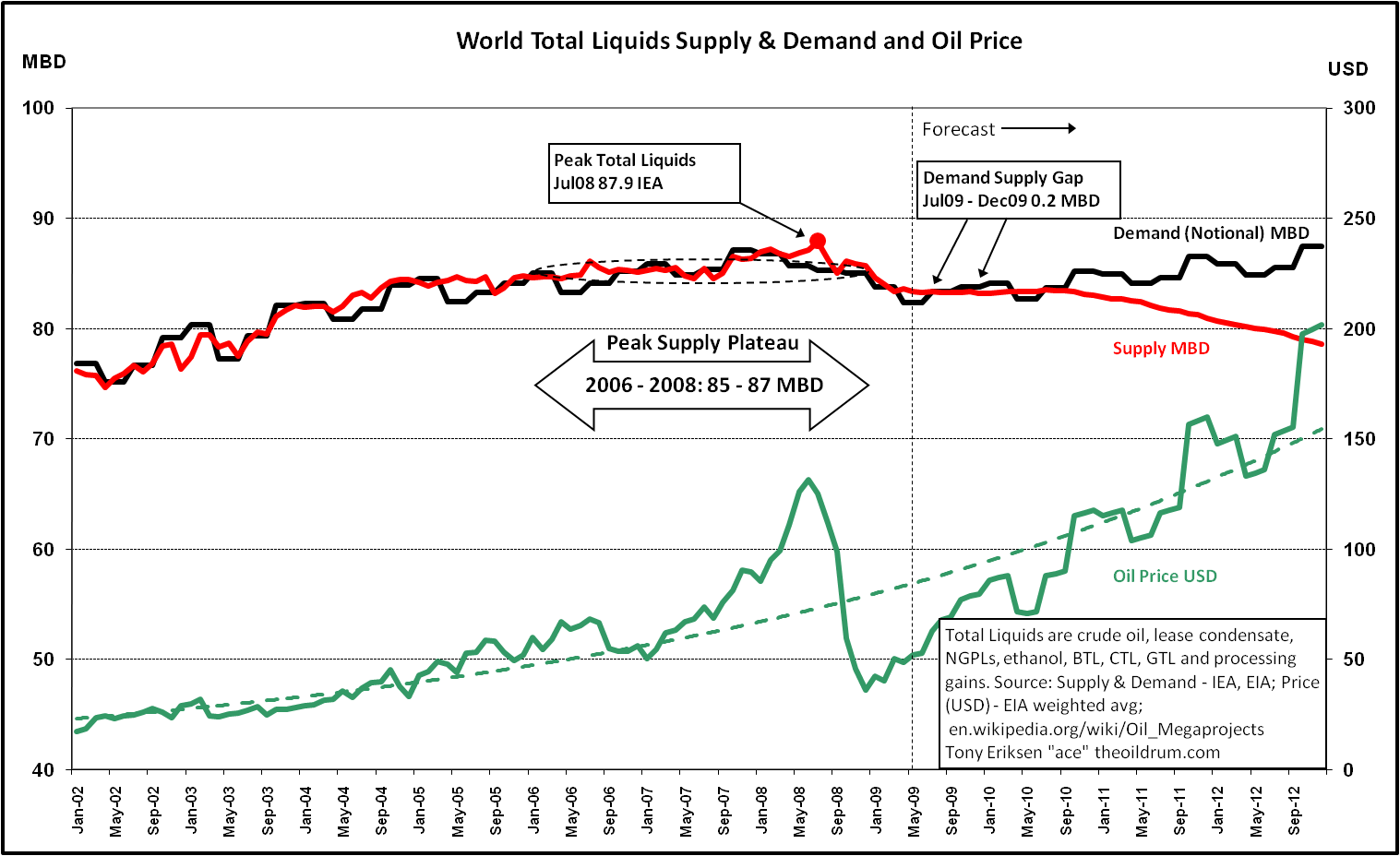

The definition of oil used by the International Energy Agency (IEA) also includes natural gas liquids (NGL), bio-fuels, processing gains and other liquids derived from natural gas and coal. OPEC NGLs were supposed to cause a significant net increase in world NGLs but this has not happened yet as NGL production is struggling to exceed 8 mbd. According to the EIA NGL data, 2007 production was 7.96 mbd, 2008 was 7.94 mbd and 2009 year to date was lower again at 7.80 mbd. Although bio-fuels production has been growing exponentially, world liquids production has probably passed peak in July 2008 at 87.9 mbd as shown below. In 2008, US ethanol production was 0.6 mbd, Brazilian ethanol production was 0.4 mbd, and bio-fuels production outside the US and Brazil was 0.5 mbd.

The average oil price should stay below $US 80/barrel for the remainder of the year as average demand is forecast to be only slightly greater than supply from July 2009 to December 2009. Furthermore, OPEC is unlikely to cut supply further which reduces the upward pressure on oil prices. Some recent evidence of increased demand is shown by US crude oil stocks dropping from a recent peak of 26.2 days at the end of April down to 25.5 days in early May. However, oil prices could exceed $100 in late 2010 as world liquids production drops further. High volatility of future oil prices is also expected due partly to delays in investment causing future oil capacity additions to decline sharply to 2012.

![]()

Sources of Future Liquids Production

There are many sources of future liquids production but it is highly unlikely that production from these sources will cause liquids production to increase above its July 2008 peak because the cumulative declines from existing crude oil production sources are too great. Key sources of future production are future discoveries. The chart below, from Colin Campbell's newsletter, shows that annual discoveries have been decreasing since the mid 1960s. It also shows that production has exceeded discoveries since 1984 which is clearly unsustainable. Campbell also forecasts future discoveries to be 110 billion barrels (Gb) which is also the number assumed for the forecasts in Fig 2 above.

Jean Laherrere also produced a discovery and production chart below from his 2008 presentation. Future discoveries, represented by the area under the dashed green line, are about 120 Gb being slightly higher than Campbell's estimate. Laherrere's discovery curve includes deepwater discoveries and also indicates that production peaked in 2008. Many of these future discoveries are likely to be either deepwater or in arctic regions. These discoveries may be significant but the time between discovery and first oil can easily be ten years which will probably not change the peak production year of 2008 but should lessen the future production decline rate.

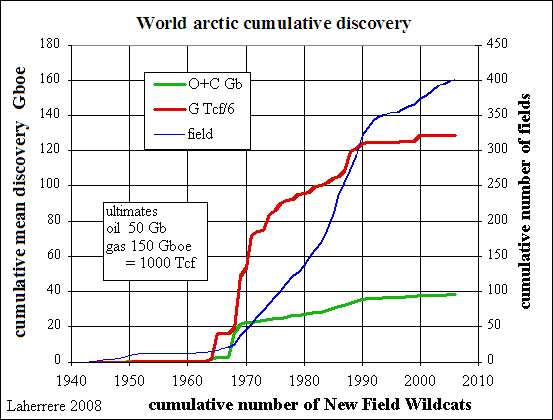

The arctic region is prospective for both oil and gas but quantities need to be estimated. Jean Laherrere estimated that the ultimate recoverable oil reserves are about 40 Gb while Colin Campbell estimates 52 Gb. There was a panel presentation at the 2009 Offshore Technology Conference (OTC.09) which discussed arctic energy challenges. One of the speakers was from Wood Mackenzie who confirmed that the arctic was prospective but mainly for gas not for oil. A report by Wood Mackenzie and Fugro Robertson estimated that the arctic will produce only about 3 percent of the world's oil and that arctic oil production, at best, would peak at 3 mbd several decades from now. Future production from the arctic region should help decrease future oil production decline rates but will probably not change the peak oil production year from 2008.

Other regions considered prospective are the US outer continental shelf (OCS) and Alaska's Arctic National Wildlife Refuge (ANWR). (Please note that the oil production potential of ANWR has also been included in the discussion above of the arctic). At this OTC.09 panel presentation on energy challenges, there was much discussion about allowing further drilling on the OCS and the ANWR. The American Petroleum Institute (API) was represented by its CEO at the panel and the API recently released this ICF report detailing potential reserves and future production from currently restricted areas in the OCS and the ANWR. This report concluded that an additional 1.1 (middle case) to 2.0 mbd (alternative case) of oil production, the majority from ANWR, might be possible by 2030 if drilling was allowed in these restricted areas. This additional production would benefit the US but would not change the peak oil date of 2008.

Canada often states that its oil reserves are almost 180 Gb. However, it is critical that 173 Gb of these reserves relate to oil sands which are not easy to produce. The chart below is from a recent presentation by the Canadian Association of Petroleum Producers and indicates the potential of Canada's total oil production to reach over 4 mbd by 2020. The forecast indicated by the red line in Figure 2 assumes that Canada oil sands production will reach a maximum of 2 mbd. Oil sands production was 1.2 mbd in 2007 and the International Energy Agency (IEA) is forecasting 2009 oil sands production to be slightly greater at 1.34 mbd. David Hughes, a Canadian geologist estimates that oil sands production will stay below 2.5 mbd due to constraints on natural gas, water and diluents. Oil sands production may reach 2.5 mbd but will not change the peak oil year.

A promising area of future liquids production is the Santos basin, offshore Brazil. There are technical challenges, explained during a Petrobras OTC.09 presentation, with the pre-salt discoveries such as very high pressures and temperatures but Petrobras is optimistic about the Santos basin, stating that this basin may almost double Petrobras' oil reserves. This implies that the Santos basin could hold as much as 15 billion barrels of recoverable oil. However, it is always important to focus on the potential future production rates in addition to the size of the reserves.

The Tupi field was discovered in November 2007 in the Santos basin and an extended well test (EWT) started in early May at a rate of 15 thousand barrels per day (kbd), to be increased to 30 kbd by the end of 2009. The Tupi EWT will run for about 16 months to better understand the flow characteristics of the pre-salt reservoir. If this EWT performs well, then a pilot test of 100 kbd should start in late 2010. If the pilot test is satisfactory then plans for full scale commercial production would be implemented. However Petrobras CFO expects a long ramp up period with Tupi peaking at over 200 kbd at the earliest in 2017. A Wood MacKenzie analyst predicted that Tupi could peak at around 1 mbd in 2022 which appears significant but Petrobras will need this increased production from the Santos basin to maintain total production at 2 mbd. The reason is that declines from existing offshore fields are about 10% or 0.2 mbd per year as confirmed by the Petrobras CFO. Future production from the Santos basin will benefit Brazil but will probably have only a negligible impact on the world production past 2012 (see Fig 2 above).

Iraq is perhaps the most promising country in the world for future potential oil production. However, it has not been an attractive country for investment not just because of terrorism but also the lack of petroleum legislation which includes national revenue sharing from the oil fields of the semi-autononous region of Kurdistan. The chart below shows that Iraq's production might reach 8 mbd by 2020 if sufficient investment was available, peace prevailed and satisfactory petroleum legislation was passed. The ultimate recoverable reserves of oil of 130 Gb is based upon Laherrere's 2003 analysis. Colin Campbell had originally forecast 4.5 mbd being reached by 2014 but now has revised that lower to 2.65 mbd in his June 2008 newsletter. In mid May 2009, the former Iraq oil minister said that Iraq's output could reach 4 mbd by 2014 and 7 mbd by 2019 if satisfactory petroleum legislation is passed in 2010. My forecast, shown by the red line in Fig 2, assumes that Iraq will produce 2.7 mbd in 2012. If the former Iraq oil minister's predictions become true then future production may be closer to the green line in Fig 2 rather than the red line. The peak oil year of 2008 would be unchanged.

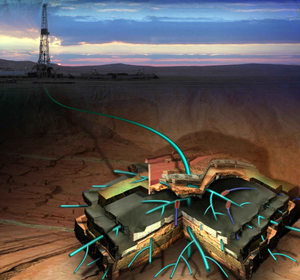

The application of advanced technology on existing discoveries is often thought to have potential for increasing production rates and recovery factors. The first production wells developed were vertical then horizontal wells became common practice. Next maximum reservoir contact wells were used for some reservoirs. Finally extreme reservoir contact wells, graphically illustrated below, are being researched by Saudi Aramco in an effort to boost recovery efficiencies. Generally, more horizontal laterals in a production well allows faster extraction of the oil but at the expense of higher production decline rates later. This recent Uppsala University report on decline rates of giant oil fields stated the following:

The important conclusion is that higher decline rates must be applied to giant fields that enter decline in the future. Prolonged plateau levels and increased depletion made possible by new and improved technology result in a generally higher decline rates. Detailed case studies of giant oilfields suggest that technology can extend the plateau phase, but at the expense of more pronounced declines in later years.

In conclusion, this analysis shows that the average decline rate of the giant oil fields have been increasing with time, reflecting the fact that more and more fields enter the decline phase and fewer and fewer new giant fields are being found. The increase is in part due to new technologies that have been able to temporarily maintain production at the expense of subsequent more rapid decline. Growing average decline rates have also been noted by IEA (2008). The difference between using a constant decline in existing production and an increasing decline rate is significant and could mean as much of a difference of 7 Mb/d by 2030.

There are other technologies such as injection to increase pressure in the reservoir. Natural gas, water, nitrogen and carbon dioxide injection can all help to maintain reservoir pressure and production rates. In 2008, Saudi Aramco injected a massive 13.7 mbd of water to maintain reservoir pressure so that 8.9 mbd oil could be produced. Fracing or fracturing the reservoir formation is another technology which can help increase production rates. The fracing can be done by forcing fluid into the formation causing fractures which are held open by special frac sand. Acid can also be used for fracing as the acid can dissolve some of the rock and increase permeability.

New technologies can extract the oil faster but can the recovery factor be increased? Schlumberger has stated that the average recovery factor for all reservoirs is about 35%. This BP study stated that the average global recovery factor is about 30-35% based on 9,000 fields from the IHS Energy database. Conversely, Saudi Aramco stated in its 2008 Annual Review that they are targeting recovery factors of 70 percent partly through the use of reservoir nano-bots known as Resbots. These Resbots would be deployed with the fluids injected into a reservoir to record pressure, temperature and fluid type which could be retrieved later in an effort to increase recovery rates. The OTC.09 Panel Presentation on Technology discussed the importance of technology and one of the presenters believed that technology will allow companies to recover over 3 trillion barrels of oil. It appears that recovery factors can be increased by using new technology but the magnitude of the increase is not clear yet. However, it is unlikely that the improved recovery factors will cause oil production to exceed its 2008 peak.

Mexico's Cantarell field is an excellent example of the use of advanced technology to stimulate the production rate, followed later by a steep decline rate. This field once produced over two million barrels per day (mbd) in 2004 and now production is less than one mbd with an annual production decline rate of over 30%. The chart below, from Matt Simmons' OTC.09 peak oil presentation, shows the steep production decline continuing into 2009. In early 2000, Pemex started using the technology of nitrogen gas injection to keep up pressure to increase production rates which was successful. However, production began to decline after 2004 and Pemex drilled horizontal wells in 2006 in an effort to extract more oil. These horizontal wells probably helped to slow the production decline rate. These technologies of nitrogen injection and horizontal wells have helped to keep production rates high. As the impact of these technologies weakens, the annual production decline rate has increased to over 30%. The expanding gas cap in the Cantarell dome continues to intersect more production wells which decreases the production rate leading to an expectation that Cantarell could become uneconomic as early as 2014.

![]()

Implications

The future sources of liquids production discussed above will help decrease the future rate of decline but it is highly unlikely that the 2008 peak will be exceeded because there are not enough countries with increasing oil production able to offset those countries with decreasing oil production. IEA oil supply warnings have been made in late 2008 when chief economist Birol said that the world needs the equivalent of four new Saudi Arabias just to maintain existing production to 2030. In April 2009, IEA's executive director Tanaka said that the world may face a crude oil shortage by 2013. As world oil production declines, consumption must also decline. Consequently, action must be taken now to reduce oil consumption and switch to alternative renewable energy sources. These sources include electricity generation from wind turbines, photovoltaic panels and geothermal sources. Other sources might be ocean energy which includes tidal energy, wave energy, thermal energy and ocean algae biofuels. Ocean thermal energy conversion was the subject of an OTC.09 panel discussion.

The IEA has recently published some recommendations to improve energy efficiency which apply not just to individuals but also to industry. For example, in the transport sector, the IEA is encouraging the use of fuel efficient tires and introducing mandatory fuel efficiency standards for light duty vehicles. In addition, this IEA document, called Energy Efficiency Policy, also encourages energy efficiency by providing links to almost 30 documents containing energy efficiency policies. One of these documents called Saving Oil in a Hurry suggests many conservation actions including increased use of public transit, car-pooling, telecommuting and speed limit restrictions. For further information, the IEA has its own energy efficiency web page. This recent Oil Drum story proposes many oil conservation ideas for individuals such as moving to a walkable neighbourhood and trading in your car for one with better mileage.

There is no simple solution to the problem of declining world oil production. A simultaneous multipronged approach will emerge which not only addresses oil conservation but also the development of alternative renewable energy sources. As oil production declines, a possible solution is to secure long term oil supply contracts ahead of the next oil price shock. China has been securing long term oil supplies from Russia, Venezuela and Iran. As oil remains critical for economic activity there is a high probability that some countries will act more aggressively in securing oil supplies, even to the extent of oil resource wars. In mid May 2009, Russia raised the prospect of war to enforce its claims on Arctic oil and gas riches.

Additional Information Sources

World Oil Production Peaked in 2008, March 17, 2009

Saudi Arabia's Crude Oil Production Peaked in 2005, March 3, 2009

Non OPEC-12 Oil Production Peaked in 2004, February 23, 2009

USA Gulf of Mexico Oil Production Forecast Update, February 9, 2009

Disclosure: The author, Tony Eriksen, has investments in the oil and gas sector. The American Petroleum Institute (API) sponsored the author's attendance to the Offshore Technology Conference (OTC.09) in Houston, Texas on May 4-7, 2009 of which the presentations reaffirmed the author's views on declining world oil production.